Key Takeaways

- Open banking APIs are booming, making them a prime target due to high-value financial data.

- Risk has shifted to exploitable API endpoints, with BOLA and auth flaws leading attacks.

- Compliance (PSD2/3, FAPI, GDPR, PCI DSS) makes API security non-negotiable.

- Security must be continuous and layered across auth, testing, and monitoring.

Global Open banking API call volumes are set to cross the 720 billion mark by 2029, and attackers know it. With the global open banking market surging past $38 billion in 2025 itself and projected to exceed $115 billion by 2030, the financial data flowing through these APIs is highly lucrative for threat actors.

With over 7.5 million calls made to just AI APIs, they have now graduated from a technical challenge to a business imperative. Since there is a serious lack of focus on developing APIs for AI and not just humans, the rising AI API calls (+40% y-o-y) create a high-movement and momentum attack surface for threat actors.

Rise in AI API call y-o-y by various LLMs (2025 State of the API Report)

Thus, as a CTO, CISO, or engineering leader at a bank or fintech, open banking API security ought to be a core element of your roadmap. That is why this guide breaks down the real risks, the regulatory maze, and the practical steps you need to build and maintain secure open banking APIs, without the jargon overload, of course.

What is Open Banking API Security, Really?

Open banking API security includes the protocols, standards, architectures, and testing practices you develop and deploy to secure your financial data as it flows between banks, third-party providers (TPPs), and end users via standardized APIs.

Think of it as a secure gateway that allows your bank to share, for example, your customer account data with a budgeting app or let a fintech firm initiate payments on behalf of a customer.

Before open banking, fintechs relied on screen scraping, where users literally handed over their banking credentials so third-party apps could log in and extract data. It was the digital equivalent of giving a stranger your house keys. Open banking APIs have replaced that mess with structured, token-based access where customers grant specific permissions without sharing any passwords.

But here’s the thing: APIs didn’t eliminate risk; rather transformed it.

Instead of worrying about credential theft at the front door, you’re now defending a standardized, well-documented interface that every attacker on the planet can study. The OWASP API Security Top 10 reads like a playbook for exploiting open banking endpoints, and 88% of API attack attempts leverage at least one of those ten methods (source).

[CTA] – Not sure where your open banking APIs stand? Talk to Astra’s certified experts for a free consultation and get started right away!

Why Open Banking APIs are High-Value Targets?

The numbers here speak for themselves. Financial services have persistently been amongst the most targeted industries for cyberattacks, with >30% of attacks exploiting public-facing applications.

Moreover, API-layer attacks specifically are accelerating at an alarming pace. With 27% of all API-focused DDoS attacks targeting financial firms in H1-2025, Salt Security found that 92% of financial services organizations experienced security problems with production APIs in the past year.

Why the bullseye? Three reasons:

- Open banking APIs carry extraordinarily valuable data: account balances, transaction histories, personal identifiers, and payment credentials.

- The standardized nature of open banking endpoints (think /accounts/{accountId}/transactions) gives attackers a predictable attack surface.

- Third, the ecosystem has an interconnected architecture. Which means that a single vulnerability can cascade across dozens of institutions.

Think of what happened with Evolve Bank & Trust. It was hit by a LockBit ransomware attack in 2024, exposing 7.6 million people’s data and sending ripples across fintech partners from Wise, Affirm, and Mercury to Stripe.

[CTA] – Your APIs are already being probed. Deploy Astra’s advanced API Security Platform Astra that helps you discover, scan, and secure each API at scale…including the zombie ones.

What are Open Banking API Security Risks?

Top of the list is Broken Object Level Authorization (BOLA). It dominates the threat landscape, accounting for roughly 40% of all API attacks financial services experience.

A deceptively simple attack, here an attacker changes an account ID in an API request, for example, swapping /api/accounts/1234 for /api/accounts/1235, and gains access to another customer’s data. How is it a risk for us? Open banking’s uniform endpoint structure makes this simple attack all the easier.

Next up is Broken authentication. Weak OAuth implementations, long-lived tokens, and missing multi-factor authentication create entry points that attackers exploit ruthlessly. Indusface’s 2025 banking security report found that weak identity controls are the single most exploited vulnerability in financial APIs.

Business logic abuse is the sleeper threat that keeps CISOs up at night. These attacks don’t trigger traditional security alerts because they exploit legitimate API functionality in unintended ways — bypassing transaction limits, replaying “first-time” flows, or calling later-stage APIs directly with crafted parameters. A payment initiation API that doesn’t enforce proper sequencing could let an attacker skip verification steps entirely.

Server-Side Request Forgery (SSRF) poses outsized risk in open banking. Salt Labs discovered a critical SSRF flaw in a major US fintech platform serving hundreds of banks and millions of customers. The vulnerability could have enabled administrative account takeover and unauthorized fund transfers across every connected institution. And excessive data exposure — APIs returning full customer profiles when only a name was requested — remains stubbornly common when filtering happens client-side rather than server-side.

[CTA] – BOLA, broken auth, SSRF…how many of these lurk in your APIs? Astra’s API security platform scans your Open Banking APIs for over 15000+ vulnerabilities. Get your first scan done today for just $7

Open Banking API Security Requirements and the Compliance Gauntlet

If you operate in open banking, you’re navigating an alphabet soup of regulations that overlap, interact, and occasionally contradict each other.

EU’s regulatory backbone, the PSD2 (and the incoming PSD3/PSR) mandates strong customer authentication that requires 2 out of 3 factors (knowledge, possession, inherence), dynamic linking that ties authentication tokens to specific payments and payees, and secure eIDAS-qualified communication for TPP identification.

PSD3, whose publication you can expect in summer 2026, expanded to include mandatory permission dashboards along with the eradication of screen-scraping fallbacks and mandated payee verification for credit transfers.

Next up, we have FAPI 2.0, which is the Financial-grade API security profile from the OpenID Foundation that reached its final specification status in February 2025. Take it as your technical blueprint for securing high-value APIs via mandating Pushed Authorization Requests (PAR), PKCE for all clients, and sender-constrained tokens via either mTLS or DPoP.

Unlike its predecessor, FAPI 2.0 has been formally verified by security researchers via a comprehensive attacker model. Colombia has already mandated FAPI 2.0, with the UK, Australia, and Brazil slowly migrating toward it.

GDPR creates tension with open banking’s data-sharing mandate. Banks must obtain explicit consent while enforcing data minimization; sharing only what’s necessary for the specific service. The 72-hour breach notification requirement applies to all API-related incidents. A Spanish bank learned this the hard way with a €6.2 million fine in 2024 for inadequate security measures under GDPR’s Article 32.

PCI DSS 4.0.1, now the only active version since April 2025, is the first PCI standard to explicitly mention APIs as requiring security controls. Requirement 6.4.2 mandates automated technical solutions deployed in front of public-facing APIs to detect and prevent attacks. Requirement 6.3.2 requires maintaining a complete inventory of all custom software including APIs and third-party components. Non-compliance carries fines of $5,000 to $100,000 per month.

[CTA] –You can’t sugarcoat or sweet-talk your compliance deadlines into extensions. Get a compliance-mapped API pentest from Astra that maps findings directly to PCI DSS 4.0.1, PSD2/PSD3, and GDPR requirements . So you’re audit-ready, not just report-ready.

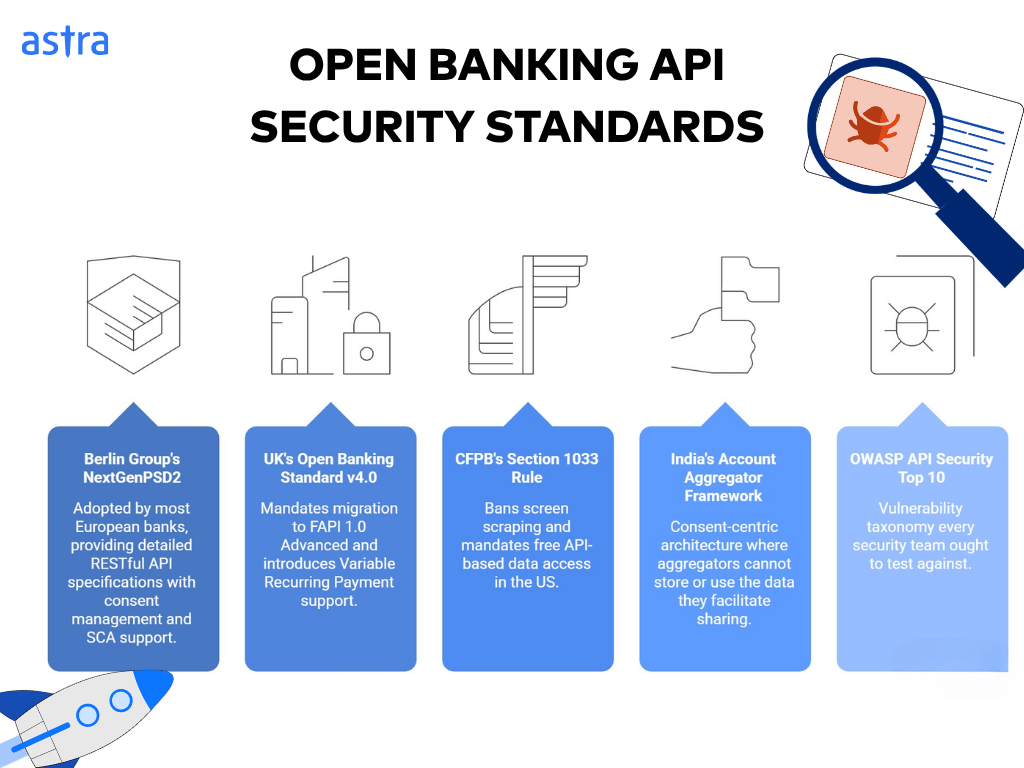

Open Banking API Security Standards and Frameworks that Actually Matter

Beyond regulations, several frameworks define the technical “how” of open banking API security.

The Berlin Group’s NextGenPSD2 framework has been adopted by almost every 3 out of 4 European banks, providing detailed RESTful API specifications with built-in consent management and support for four SCA models (redirect, OAuth2, decoupled, embedded). Also, the UK’s Open Banking Standard v4.0, which was published in 2024, mandated migration to FAPI 1.0 Advanced before 2025 and introduced the Variable Recurring Payment support.

The US, on the other hand, has the CFPB’s Section 1033 rule (finalized October 2024) that bans screen scraping and mandates free API-based data access. This is a huge shift for the American market, where only 36 unique open banking APIs exist compared to the UK, which hosts north of 196.

India’s Account Aggregator framework has scaled to 120 million linked accounts with a consent-centric architecture where aggregators can never store or use the data they facilitate sharing.

Moreover, OWASP API Security Top 10 (2023 edition) still serves as the vulnerability taxonomy every security team ought to test against. Why? Well, 88% of attack attempts still map to this list, making it essentially the starting point of your testing checklist.

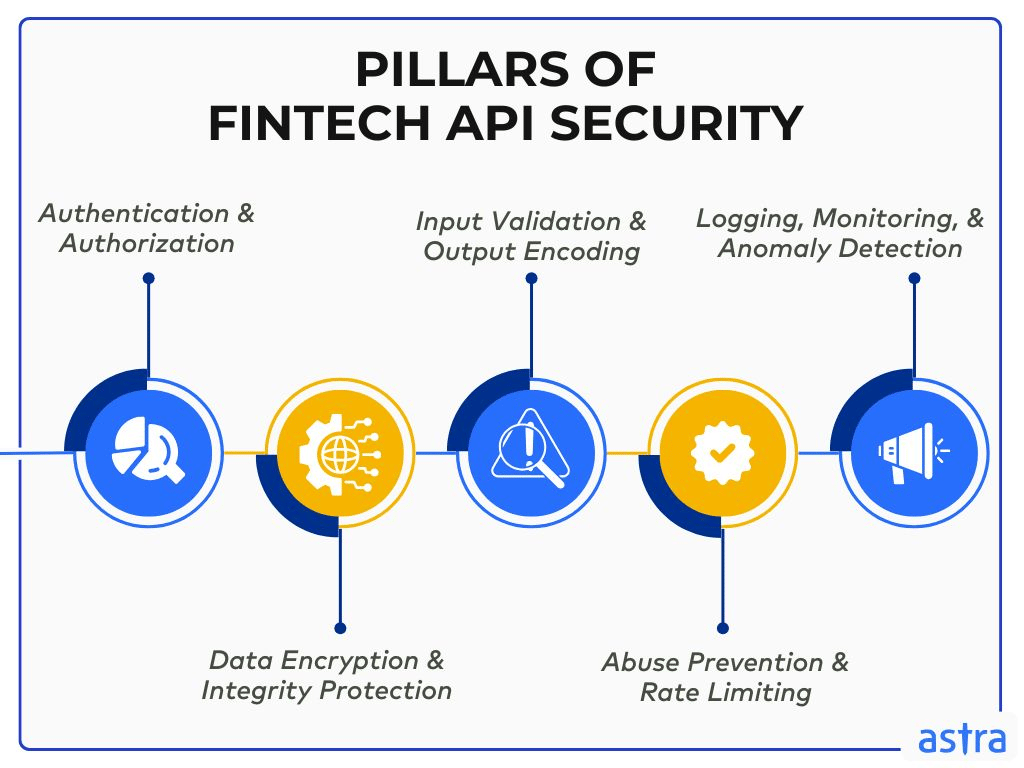

Best Practices for Securing Open Banking APIs

Being practical would mean zeroing in on secure open banking implementations that don’t inadvertently or otherwise give you breach headlines. Below, we try to summarize the core ones:

Authentication and token management

They are your first line of defense, requiring you to implement OAuth 2.0 with PKCE for all authorization flows. This eliminates authorization code interception attacks. Use Pushed Authorization Requests to move sensitive parameters off the browser to server-to-server channels.

Sender-constrain your tokens: mTLS for confidential server-side clients, DPoP for mobile and single-page applications. Keep access tokens short-lived and implement robust refresh token rotation.

Your API gateway must do the heavy lifting

- Enforce schema validation against your OpenAPI specification before traffic reaches backend services.

- Implement granular rate limiting based on client, endpoint, and user using sliding window algorithms rather than just fixed windows to prevent burst abuse.

- Lastly, validate content types rigorously since an API that’s secure against JSON injection may be vulnerable when the same endpoint accepts XML.

Consent management deserves its own architecture

- Build dedicated consent APIs with full lifecycle support: grant, update, revoke, and audit.

- Every data access must be time-limited to customer-defined parameters.

- Provide real-time consent dashboards and ensure revocation triggers immediate system-wide updates. Under GDPR and the coming PSD3, this isn’t optional.

Encryption needs to be comprehensive

- This entails TLS 1.3 with Perfect Forward Secrecy for all data in transit

- AES-256 for data at rest, and tokenization needs to replace sensitive values like PANs and PII wherever possible.

- Store cryptographic keys in hardware security modules (HSMs) and make sure these keys are rotated regularly.

- For forward-looking teams, NIST now recommends evaluating hybrid post-quantum cryptography models, all thanks to the rise in “harvest now, decrypt later” threats.

Logging and monitoring close the loop

- Maintain immutable audit logs and record every data access event that includes identity, timestamp, data accessed, and policy decision.

- Integrate these with your SIEM platform to build behavioral thresholds for everyone that utilize your API.

- ML-powered anomaly detection can flag deviations, such as excessive token refresh attempts, unusual geographic patterns, and abnormal request volumes, before they become breaches.

[CTA] – Fail-proof your APIs and find vulnerabilities that other pentests often miss with our AI-infused API Penetration Testing. Start today

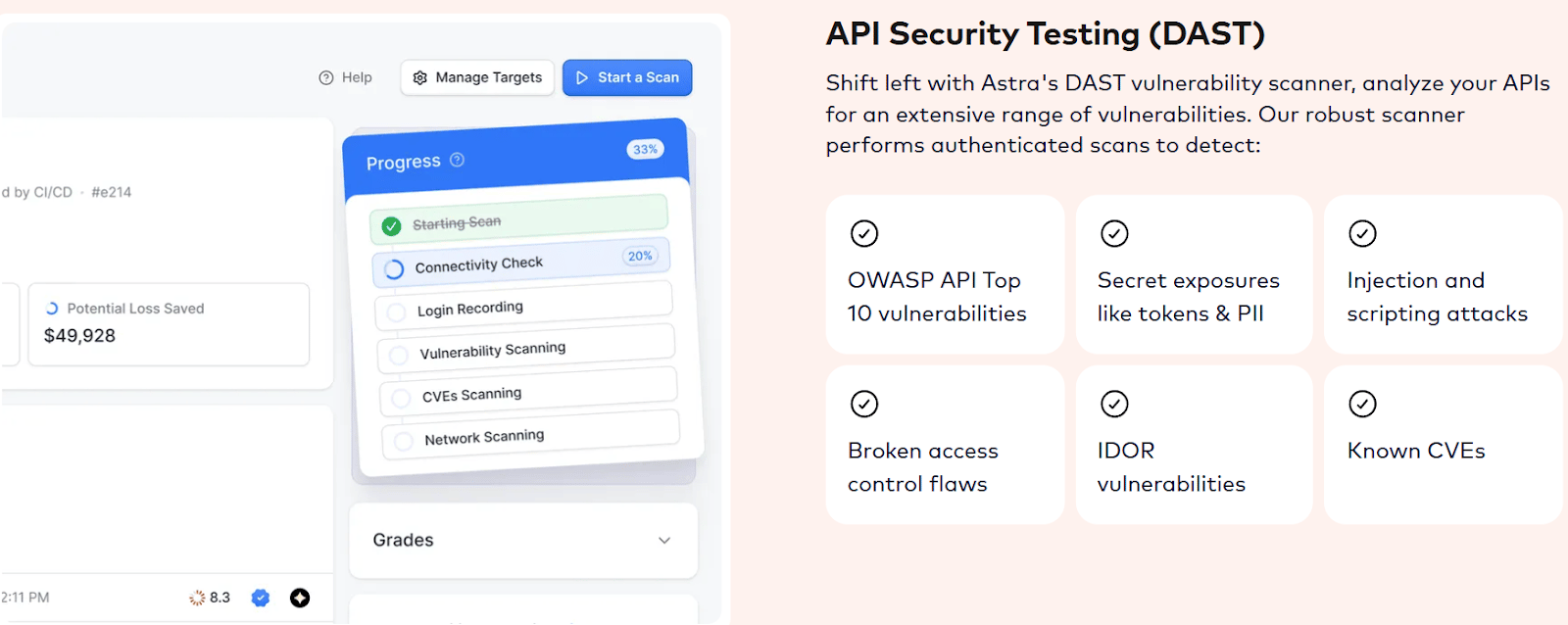

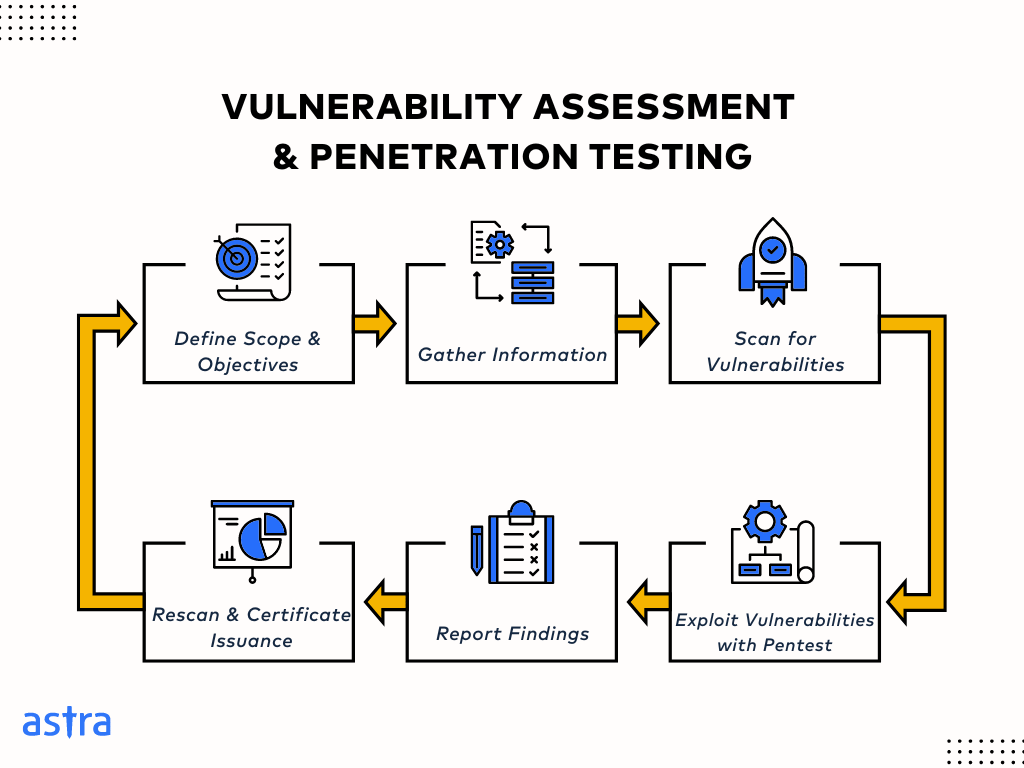

Open Banking API Security Testing and Validation

Testing financial APIs demands a layered approach that involves continuous API VAPT. Below, we discuss in brief what to include while testing and validating your open banking API security posture.

Penetration Testing

This starts with mapping directly to the OWASP API Security Top 10, such as BOLA broken authentication and business logic flaws specific to financial workflows.

Here, both black-box and grey-box methodologies are essential as the former simulates external attackers while the latter reflects the reality that TPPs have API documentation and some access credentials. Moreover, PCI DSS 4.0 now requires quarterly vulnerability scans and annual penetration tests, plus additional testing after significant changes.

[CTA] – Astra API Security Platform best marries offensive testing with live traffic intelligence to offer complete API observability via 15000+ DAST test cases and compliance-ready risk classification & scoring. Check it out now!

API-Specific Fuzzing

This helps uncover edge cases that structured testing misses. This is done via Schema-aware fuzzers that read your OpenAPI specification automatically and generate endpoint-specific test payloads, mutating valid inputs to trigger unexpected behavior.

This becomes indispensable for your financial APIs, where boundary conditions in transaction amounts, date ranges, and account identifiers can expose vulnerabilities.

Remember to never fuzz production environments and always use staging mirrors that too with sanitized data.

Dynamic Application Security Testing (DAST)

This helps catch runtime vulnerabilities before deployment across your CI/CD pipeline. Modern API-specific DAST tools send malicious payloads, manipulate inputs, and analyze responses without requiring source code access.

Do notice that most DAST scanners miss API endpoints that aren’t exercised by the frontend. You need an Open Banking API Security vendor that tests endpoints directly based on your API specification.

Runtime protection is your final safety net. RASP (Runtime Application Self-Protection) embeds security into the application itself and for financial APIs where zero-day exploits target business logic, RASP offers application-context awareness that gateways and WAFs lack.

The winning formula here is layered coverage: SAST during development, automated DAST in CI/CD, periodic manual penetration testing for critical endpoints, and continuous behavioral monitoring in production.

Third-party and Fintech Integration Risks in Open Banking API Security

41.8% of fintech breaches originate from third-party vendors, according to SecurityScorecard. Moreover, we can barely ever forget the Evolve Bank breach, in which a single employee clicked a phishing link, and the resulting LockBit ransomware attack exposed data across the entire Banking-as-a-Service ecosystem.

What needs to be addressed here is regulatory asymmetry. Under PSD2, once a TPP receives regulatory authorization, banks must grant API access.

But financial institutions cannot make access contingent on independently testing the TPP’s security posture. Burgeoning and thinly capitalized fintechs may have the same data access rights as major institutions, but can’t afford a similar security infrastructure to protect that data.

Mitigating third-party risks when it comes to Open Banking APIs mandates ongoing verification:

- Monitoring the validity of the TPP certificate

- Tracking regulatory authorization status across jurisdictions (58% of EEA TPPs operate cross-border)

- Enforcing data minimization at the API level

- Maintaining contract-based security requirements that are robust in terms of incident response

Building a Secure Open Banking API Security Architecture

Here again, you need a layered pattern:

- TPP clients connect through an API gateway that handles mTLS termination, token validation, rate limiting, and schema enforcement.

- Next, behind the gateway, dedicated microservices handle authentication, consent management, and business logic (each communicating via encrypted and mutually authenticated channels)

Secondly, zero-trust principles need to govern every layer where you authenticate and authorize every API request, regardless of origin. Moreover, make sure APIs receive only the permissions they need.

Next up is Micro-segmentation. It restricts API-to-API communication to explicitly permitted paths, preventing almost any compromised payment-processing service from reaching the customer onboarding API.

Data isolation becomes crucial in multi-tenant environments. Here, you need per-tenant encryption keys that are managed through cloud KMS, row-level security at the database layer, and automated metadata tagging.

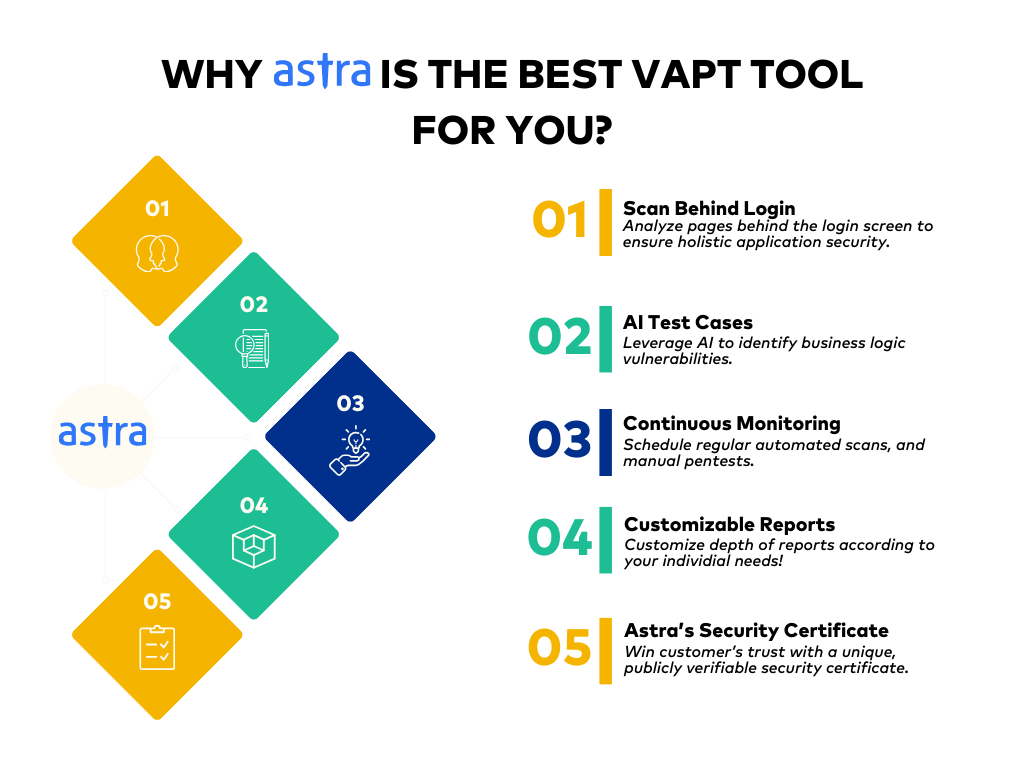

How to Choose an Open Banking API Security Partner?

Look, not all security solutions can cater to the unique demands that APIs have, especially when it comes to Open Banking, which is much more vulnerable and lucrative for threat actors. Thus, when evaluating partners, look for these capabilities:

Firstly, API-specific expertise matters enormously. Generic web application security tools miss the nuances of OAuth token flows, consent lifecycle management, and financial business logic. Your partner should understand FAPI security profiles, eIDAS certificate validation, and the specific attack patterns targeting banking APIs — not just OWASP’s general web vulnerability list.

Second, demand continuous vulnerability assessments and penetration testing (VAPT). Why? Open banking APIs evolve constantly with new endpoints, TPP integrations, and regulatory requirements, and thus a partner that can offer only annual penetration tests or vulnerability scans leaves you exposed for 364 days. Also look for DAST in CI/CD, runtime protection, and ongoing monitoring.

Third, regulatory fluency is non-negotiable. Your security partner should map findings directly to PCI DSS 4.0.1, PSD2/PSD3, and GDPR mandates. It should also produce compliance-ready reports. Moreover, the ability to test against FAPI 2.0 conformance requirements is now high-stakes.

Fourth, evaluate the depth of business logic testing. Automated scanners catch injection attacks and misconfigurations. What separates strong partners is the ability to identify weaknesses in authorization bypass, payment flow manipulation, and consent management that require human expertise to uncover.

Finally, consider ecosystem coverage. Financial institutions manage an average of 601 APIs (F5 2024). Shadow and zombie APIs — undocumented or deprecated endpoints still running in production — are among the most dangerous attack surfaces. Your partner should offer API discovery and inventory management, along with active testing.

Future Trends in Open Banking API Security?

AI-Driven Threat Detection

The buzzword everyone’s chasing isn’t just a buzz; HSBC, in its partnership with Google Cloud, has reduced false positives by 60% using ML-powered fraud detection. Graph neural networks map relationships across billions of records and identify fraud networks spanning multiple institutions.

The next frontier, i.e., agentic AI will involve autonomous systems that’ll correlate signals across telecom, banking, and device data for real-time threat response.

Decentralized Identity

This can fundamentally change how open banking handles authentication. W3C’s Decentralized Identifiers (DIDs) and Verifiable Credentials have enabled reusable KYC — one bank issues a verified credential, and others accept it instantly without re-verifying identity.

PSD3 and Global Regulatory Convergence

With 78 countries now implementing open banking regulations, the compliance complexity will grow, driving the need for harmonized standards. FAPI 2.0’s adoption as a global baseline and DORA’s operational resilience requirements in the EU show the torch to a future where API security isn’t just a technical decision but a board governance obligation.

Thus thick firewalls aren’t gonna help you sustain. You need to treat your Open Banking API security as a continuous, adaptive discipline that is embedded in your architecture, development pipeline, and organizational culture. You can’t just break the trust of >183 million open banking users, you’ve got to move one secure API call at a time.

[CTA] – Astra Pentest is built by the team of experts who helped secure Microsoft, Adobe, Facebook, and Buffer. Start with a free consultation from Astra Security — and build the kind of security posture that earns trust at scale.

FAQs

Is Open Banking API free?

For the end customer, yes, not for the fintech firms and companies providing that service by either outsourcing it or building in-house.

How Secure are Open Banking APIs?

They are more secure than the screen-scraping methods they replaced as they use token-based access, strong customer authentication, and standardized protocols like OAuth 2.0 and FAPI 2.0.

What are the risks in Open Banking API?

The main risks in open banking APIs include Broken Object Level Authorization (BOLA), Broken authentication via weak OAuth implementations, Business logic abuse that bypasses transaction controls, Server-Side Request Forgery (SSRF), and Excessive data exposure.