TLDR;

- PCI DSS data security standard is a set of mandatory rules that govern how every organization should accept, process, transmit, and store card data to prevent fraud and data breaches. It was developed in 2004 by major credit card companies – Visa, American Express, JCB, and Discover.

- Four compliance levels determine your audit frequency and other obligations based on transaction volume.

- The standard is built on 12 requirements spanning network security, data protection, access control, monitoring, and organizational policy.

- Non-compliance can trigger $5,000 – $100,000 in monthly fines, forced audits, and termination of card processing rights.

- Modern IT infrastructure introduces specific compliance gaps that require deliberate architectural changes.

- Third-party vendor sprawl is one of the overlooked sources of PCI DSS scope exposure.

For a standard built in 2004, PCI DSS still decides the fate of modern payment systems. However, here’s the paradox: the businesses that fear it most are often already more secure than those that treat it as routine.

With the attack surface expanding rapidly in 2026, driven by AI implementations and increasingly complex cloud-native environments, this guide cuts through outdated assumptions, breaks down what actually matters today, and shows you how to use PCI data security standards as a lever in online payment security rather than a limitation.

What is the PCI Data Security Standard?

PCI DSS is a global security framework to protect cardholder data and secure payment transactions. It applies to any business that involves card transactions, regardless of size.

PCI DSS is administered by the Payment Card Industry Security Standards Council(PCI SSC), founded on September 7, 2006. Visa, Mastercard, American Express, Discover, and JCB jointly established the council to standardize payment security across the industry.

The standard addresses two core objectives

- Secure card transactions

- Procet the PII of cardholders

Why Astra is the best in pentesting?

- We’re the only company that combines automated & manual pentest to create a one-of-a-kind pentest platform.

- Vetted scans ensure zero false positives.

- Our intelligent vulnerability scanner emulates hacker behavior & evolves with every pentest.

- Astra’s scanner helps you shift left by integrating with your CI/CD.

- Our platform helps you uncover, manage & fix vulnerabilities in one place.

- Trusted by the brands you trust like Agora, Spicejet, Muthoot, Dream11, etc.

Whom does PCI DSS apply to?

The PCI DSS applies to any organization that stores, processes, or transmits cardholder data or sensitive authentication data, regardless of size or transaction volume. Compliance obligations fall on payment providers and their customers, not on PCI SSC.

In simple terms, if your business handles payment cards from Visa, Mastercard, American Express, Discover, or JCB, you must comply with PCI DSS. The standard is mostly enforced by card brands through your acquiring bank.

- Merchants – Any business that accepts payment cards, whether in-person or online.

- Service Providers – Companies that process, store, or transmit card data on behalf of merchants (e.g., payment gateways, processors, cloud hosting providers, tokenization services).

- Financial institutions – Entities that are involved in the payment ecosystem.

- Third-party vendors – Any Entity that can impact the security of cardholder data.

Why is PCI DSS Compliance Important?

PCI DSS compliance is important because it gives organizations a repeatable security baseline. It limits access, secures cardholder data, and enforces regular security testing, things that any payment-handling system needs to be secure.

Beyond avoiding fines, PCI compliance delivers immense operational value.

- Builds accountability into systems before security debt accumulates

- Reduce ambiguity while making security-related decisions across multiple teams.

- Establishes minimum security expectations for third-party tools and vendors

- Paves the way for business deals with enterprises

What are the 4 PCI DSS Compliance Levels?

PCI DSS 4.01 defines four merchant compliance levels based on the volume of annual transactions. Each level specifies different rigor and methods of PCI DSS compliance validation. The PCI Security Standards Council (PCI SSC) defines the core PCI DSS requirements, but the individual card brands set and enforce the merchant-level criteria and validation.

Level 1

Applies to merchants processing more than six million worldwide credit or debit card transactions per year, or any merchant that has been identified as Level 1 by a card brand or has suffered a data breach recently.

Validation requirements for Level 1 PCI DSS:

- Annual on-site assessment by a Qualified Security Assessor (QSA) resulting in a Report on Compliance (ROC)

- Attestation of Compliance (AOC)

- Quarterly network vulnerability scans by an Approved Scanning Vendor (ASV)

This is the strictest level and is usually applied to large enterprises or global retailers.

Level 2

Level 2 applies to merchants processing between 1 million and 6 million credit or debit card transactions per year.

Validation requirements for Level 3 PCI DSS:

- Annual Self-Assessment Questionnaire (SAQ)

- Attestation of Compliance (AOC)

- Quarterly ASV scans may be required, depending on the card brand and your acquiring bank.

Level 3

Applies to merchants that process 20,000 to 1 million transactions(card-not-present) each year.

Validation requirements for Level 3 PCI DSS:

- Annual Self-Assessment Questionnaire (SAQ)

- Attestation of Compliance (AOC)

- Quarterly network vulnerability scans by an Approved Scanning Vendor (ASV)

Level 4

The lowest level of PCI compliance applies to organizations with fewer than 20,000 e-commerce transactions per year, or those that process up to one million real-world transactions(across all channels)

Validation requirements for Level 4 PCI DSS:

- Annual Self-Assessment Questionnaire (SAQ)

- Attestation of Compliance (AOC)

- Quarterly ASV scans are often required or strongly recommended by the acquiring bank.

No other pentest product combines automated scanning + expert guidance like we do.

Discuss your security

needs & get started today!

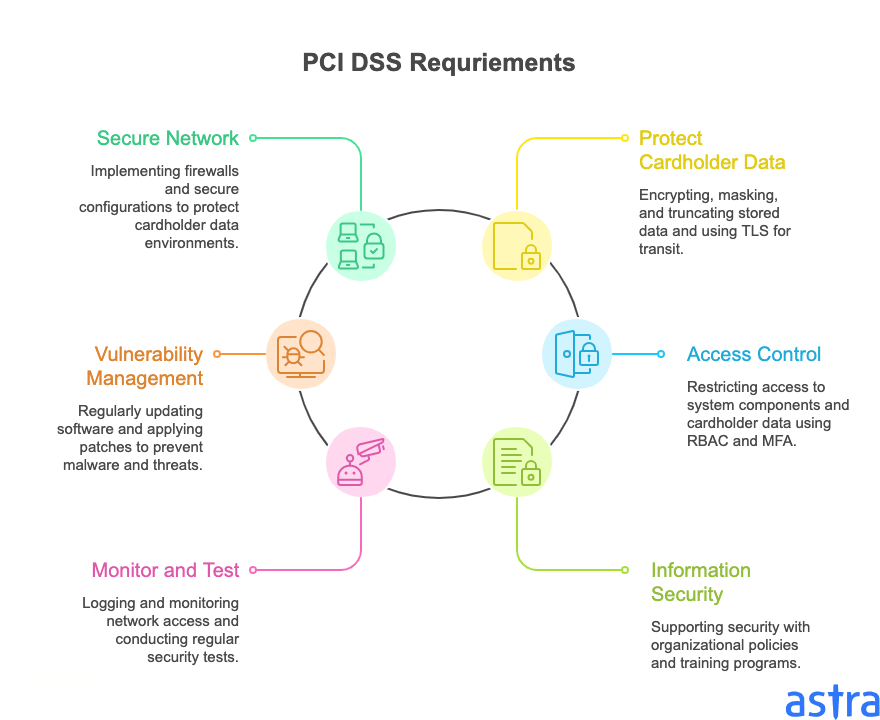

What are the PCI DSS Requirements?

PCI DSS compliance is structured around 12 core requirements grouped under 6 security goals. Every requirement is mapped to a testable control that organizations must implement and maintain

Goal 1: Build and Maintain a Secure Network

- Requirement 1: Install and maintain network security controls (e.g., firewalls) and access rules to protect cardholder data environments.

- Requirement 2: Apply secure configurations to all system components.

Goal 2: Protect Cardholder Data

- Requirement 3: Protect every stored account data by encrypting, masking, or truncating. Avoid storing sensitive authentication data after authorization.

- Requirement 4: Protect the cardholder in transit by using strong TLS encryption.

Goal 3: Maintain a Vulnerability Management Program

- Requirement 5: Protect systems from malware and other threats by regularly updating and deploying antivirus software or software to detect malicious activity.

- Requirement 6: Develop and maintain secure systems by applying patches, implementing secure coding practices, and having a proper vulnerability management program

Goal 4: Implement Strong Access Control Measures

- Requirement 7: Restrict access to system components and cardholder data, and implement role-based access control (RBAC).

- Requirement 8: Identify and authenticate access to system components by using unique IDs, MFA, and session timeouts.

- Requirement 9: Restrict physical access to cardholder data (limit and monitor access to data centers and hardware)

Goal 5: Monitor and Test Networks

- Requirement 10: Log and monitor all access to network resources and cardholder data through SIEM tools with a tamper-evident audit

- Requirement 11: Test the security of systems and networks regularly (run internal/external scans, conduct pentests)

Goal 6

- Requirement 12: Support information security with organizational policies and programs (maintain an active security policy and training programs)

What are the Penalties for PCI Compliance Violations

PCI DSS is not a government regulation, so it does not trigger government fines.

Non-compliant merchants could face monthly fines ranging from $5,000 to $100,000 per month until compliance is demonstrated. The exact amount depends on the volume of card data at risk.

Non-compliance can also trigger forced audits, higher processing fees, or even get your ability to process cards revoked, a deal-breaker for most businesses. Even small businesses (Level 4) can face significant financial consequences.

And if there’s a breach? You’re covering legal fees, investigation costs, and customer fallout, often with far more damage to your brand than to your balance sheet.

Challenges & Best Practices for Keeping Up with PCI DSS

.PCI DSS compliance remains technically demanding due to the need for precise scoping, continuous control validation, and alignment with evolving requirements in PCI DSS 4.0.1. Organizations often underestimate the complexity of maintaining a secure cardholder data environment (CDE) while balancing business operations. These challenges account for the majority of the audit failures.

1. PCI controls were not designed for a dynamic infrastructure

PCI DSS was written for static, on-premise server environments. The use of standard language, i.e., ‘system components’, ‘servers’, reflects older architectures. Applying those to modern containerized and cloud environments is tough. This challenge pops up when defining the scope for controls.

Expert Recommendations

- Define your CDE boundary at the architectural level.

- Use policy-as-a-code tools to enforce PCI controls at the infrastructure level.

- Map PCI controls to their security intent.

2. Security and compliance operate in silos.

In most organizations, PCI compliance is often handled only by the compliance team or legal without engineering or other teams’ involvement. Product teams and other teams are involved only when it blocks a release, stalls a business deal, or triggers an audit finding. This creates a patchwork or temporary controls that satisfy the audit on paper but fail under real world scneanios3

Expert Recommendations

- Assign ownership to the engineering teams responsible for systems under PCI controls.

- Rune tabletop exercise with security, compliance, and engineering teams to simulate realistic breach scenarios.

- Make PCI DSS scope review mandatory in system design.

3. Third-Party Vendors Expand Your PCI Scope

Organizations do not need to directly mishandle card data to fall out of PCI DSS compliance. Even third-party vendors and integrations can expose card data without internal teams detecting it. So every third-party vendor, tool, or service that touches your card data environment is in PCI DSS scope. This even includes analytics platforms that capture form input, CS tools, and marketing integrations with access to card data.

Expert Recommendations

- Have a decommissioning process for vendor integrations when they fall out of PCI DSS scope.

- Keep a live, continuously updated inventory of all services, vendors, or tools that have access to or influence your cardholder environment (CDE).

- Ask for PCI DSS compliance attestations or a current SAQ/ROC from every vendor that has access to your card data.

Best Practices for PCI DSS Compliance

Effective PCI DSS compliance is about building and maintaining controls that hold up in real-world conditions year-round. Organizations that treat PCI DSS as a continuous security discipline achieve better protection and lower long-term costs compared to those that only prepare for audits.

1. Build compliance into the architecture

The most expensive PCI DSS remediation projects occur when compliance is ignored during initial system design. Retrofitting controls such as tokenization, strong encryption (AES-256), least-privilege access models, centralized logging (SIEM), and proper network segmentation becomes significantly more complex and costly.

Introduce PCI DSS scope review as a mandatory gate in your system design process.

2. Automate Control Enforcement

Manual processes are prone to human error and fail to scale in complex environments.

Any PCI DSS control that depends on people remembering to do something will eventually fail (e.g., running a scan, rotating a key, reviewing an access list, etc.) The goal is to make compliance the path of least resistance.

3. Run penetration tests

PCI DSS requires annual penetration testing of the cardholder data environment at both network and application layers (Requirement 11.4). However, best practice goes beyond the minimum: perform authenticated and unauthenticated tests, include social engineering simulations where appropriate, and conduct testing after any significant infrastructure or application changes.

Tests must be carried out by a qualified internal or external party with appropriate certifications.

4. Minimize Scope Through Tokenization

The most effective way to reduce compliance burden is to minimize or eliminate the cardholder data environment. Implement tokenization services, point-to-point encryption (P2PE), or fully outsource payment processing to PCI DSS Level 1 service providers. This approach can dramatically reduce the number of systems, networks, and people in scope.

How Can Astra Help as a PCI ASV?

Astra functions as a PCI Approved Scanning Vendor (ASV), offering external vulnerability scans that meet PCI DSS requirements for internet-facing systems in scope. Our platform supports modern environments, including cloud infrastructure, APIs, and applications behind authentication

.

Astra Security’s continuous pentesting platform can satisfy PCI DSS Requirements 11.3.2 and 11.4, which mandate external scanning and penetration testing without requiring a separate compliance workflow alongside the engineering process.

Scans are manually validated by security engineers to eliminate false positives. Two rescans are included, allowing teams to remediate and verify fixes before final submission. Reports meet PCI ASV format standards and can be shared via a public Trust Centre.

With seamless integrations of CI/CD and ticketing tools, such as Jira, GitHub, GitLab, and Jenkins, to streamline remediation. A central dashboard tracks scan history, issues, and status across assets, with dedicated support available throughout the compliance cycle

Astra Pentest is built by the team of experts that helped secure Microsoft, Adobe, Facebook, and Buffer

Final Thoughts

PCI data security standard isn’t going away. It’s still the baseline for anyone touching payment data, and while it may feel dated next to today’s tech stacks, it’s one of the few standards that still carries real weight when something breaks.

The harder part is execution, figuring out what’s actually in scope, getting meaningful tests done, and avoiding last-minute scrambles when an audit lands. Most of the frustration with PCI stems from how it’s handled, rather than what it requires.

Done right, PCI isn’t overhead. It’s just part of how you ship and scale responsibly.

FAQ

1. Is PCI DSS a legal requirement?

PCI DSS is not mandated by governments; rather, it’s a contractual requirement enforced by major card networks and acquiring banks. Failure to comply carries financial penalties and can result in loss of card processing privileges.

2. What is the difference between PCI DSS and PA-DSS?

PCI DSS governs how organizations handle their cardholder data, while PA-DSS governs the security of payment applications themselves. PA-DSS was superseded by the Software Security Framework(SSF) in 2022.

3. How long does PCI DSS certification take?

Timeline varies by the compliance level and organizational readiness. Completing a self-assessment questionnaire (SAQ) for level 4 can be done in days or weeks. Level 1 merchants undergoing QSA audit may take more than 3 months of preparation, depending on the volume of their cardholder environment and the complexity of their IT infrastructure.

4. Does Tokenization remove the need for PCI DSS compliance?

Tokenization can reduce the scope of PCI DSS by replacing card data with non-sensitive tokens. But it doesn’t eliminate compliance obligations entirely. Any system that is involved in the tokenization process or card data remains in the PCI DSS scope.